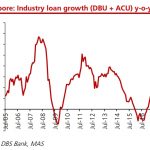

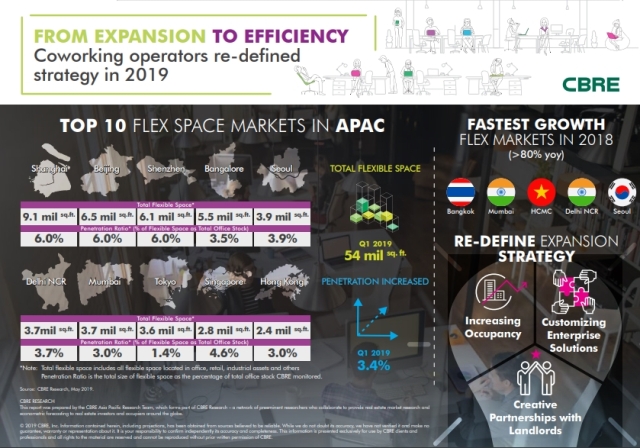

Flexible space continues to proliferate across Asia Pacific, reaching a total footprint of 54 million sq. ft. as of March 2019, accounting for more than 3% of total office stock, said a recent research by CBRE. The report said that Shanghai still possesses the largest volume of flexible office space but Indian and Southeast Asian markets are recording the fastest growth.

As flexible space operators have already built critical mass for their service offering, CBRE expects 2019 to herald a shift in strategy from expansion to efficiency. This will include a focus on the following.

- Raising occupancy: Attract new and repeat members, increase space densities, and shorten sales cycles to achieve desired occupancy.

- Customising enterprise solutions: Target corporate occupiers and customise service and product offerings to cater to this demand.

- Form creative partnerships with landlords: Partner with landlords via management contracts to enhance agility in their portfolios.

Singapore is among the megacity forerunners for total flexible space with 2.8 million sq.ft. with penetration Ratio of (% of Flexible Space as Total Office Stock) 4.6 per cent said the report.

Table of Contents

In another report, CBRE said that news of a potential WeWork (We Company) IPO is placing the flexible-office-space sector front and center.

The We Company, commonly known as WeWork, says its mission is to “elevate the world’s consciousness.” Its core business is leasing office real estate and then subleasing that office space to individuals and small companies who can’t commit to a traditional office lease.

https://www.icompareloan.com/resources/flexible-workspace/

CBRE said that while questions have been raised about the profitability of these operators in a recession, it is unquestionable that the meteoric growth of the flexible space sector is unprecedented in commercial real estate.

CBRE said that this is what it knows about the flexible space sector today (based on the 30 markets tracked by CBRE):

“

- The top-10 markets account for more than 70% of the nation’s flexible-office inventory (25% in Manhattan alone). With nearly 4 billion sq. ft. of traditional office space in the 54 major metros tracked by CBRE, continued growth of flexible space is inevitable even under conservative estimates.

- In 2018 alone, flexible space in the top-10 markets grew by 25%, with Manhattan growing the most on an absolute basis (+4 million sq. ft.) and Seattle growing the most on a percentage basis (44%). Growth since the start of this cycle has been constant and is showing no signs of slowing. Flexible-space operators are currently in the market for more than 6 million sq. ft. of space.

- Flexible space as a percentage of total office inventory is around 2%, with San Francisco and Manhattan being the most saturated (over 3% each). In some foreign markets, such as London and Beijing, flex space accounts for more than 5% of total office inventory.

- Only 15 markets have more than 1 million sq. ft. of flexible-office inventory. Many U.S. markets have not even scratched the surface of this sector, including high office-using employment growth markets like Nashville, Austin and Charlotte.

- The top-five operators by square footage are WeWork, Regus, Spaces, Knotel and Industrious. The We Company (WeWork) and IWG (Regus and Spaces) hold 50% of the U.S. flexible-office inventory. Knotel and Industrious have another 10%.

- The Fortune 500 is engaged and intrigued. 85% of real estate executives plan to implement flexible-office solutions into their portfolio strategy, according to the 2018 Americas Occupier Survey. Enterprise customers are early in the implementation stage of flexible-office solutions as a portfolio strategy. If these strategies prove successful, there is potential for more explosive growth of coworking.

- The top flexible-space markets are also the highest for technology industry growth and office rent. With many coworking operators expanding in these mature markets, there are valid questions about their potential profitability. Those that deliver a well-operated, experiential product will have the best chance to achieve good margins.

- Despite the rise of flexible office space, there was still more than 19 million sq. ft. of small, traditional-office deals (under 5,000 sq. ft.) transacted last year in the top-20 markets. And there is more than 140 million sq. ft. of space coming up for renewal over the next 24 months in these markets (more than half of them for 50,000 sq. ft. or less). Given these statistics, there is clearly more market share to be gained.

- CBRE Research found that nearly 40% of office building sales with some flexible-space component achieved values greater than the average for office buildings in their markets that had no flexible-space component. Higher capitalization rates seem to correlate with higher amounts of flexible space occupancy—a signal that long-term lease commitments are still preferred by investors, yet a portion of flexible space is acceptable to them.

- The flexible leasing trend is not limited to offices: Medical labs, industrial facilities, housing and retail are promising areas to watch. Niche operators catering to specific businesses or demographics also are emerging. There is potential for diversification of coworking across niche players, asset types and geographic submarkets.

“

https://www.icompareloan.com/resources/singapore-office-rents/

CBRE noted that although there remains many questions to answer, the facts highlight that coworking will likely achieve much more growth. It added that perhaps the structure of how flexibility is presented to tenants will change; but that it is evident that flexible space offerings will be a long-term feature of the commercial office market because of the value they provide to a broad range of occupiers.

How to Secure a Commercial Loan Quickly

Are you planning to purchase a similar prime commercial redevelopment site but unsure of funding? Don’t worry because iCompareLoan mortgage brokers can set you up on a path that can get you a commercial loan in a quick and seamless manner.

Alternatively you can read more about the Best Commercial Loans in Singapore before deciding on your purchase. Our brokers have close links with the best lenders in town and can help you compare Singapore commercial loans and settle for a package that best suits your commercial purchase needs. Our services are also very personalised and tailored to the unique needs of the buyers.

Whether you are looking for a new commercial loan or to refinance and existing one, our brokers can help you get everything right from calculating mortgage repayments, comparing interest rates, all through to securing the final loan. And the good thing is that all our services are free of charge. So it’s all worth it to secure a loan through us for your next purchase.

If you need advice on a new commercial loan or Personal Finance advice.

If you want to speak to our trusted Panel of Property agents.

If you need refinancing advice.