By Ku Swee Yong, Paul Ho

This article has also been featured on The Edge Property

Residential property prices have softened by 7% over the last two years. A common question we hear these days is, “Should I buy now?”

Given all the facts about the oversupply of residential properties, high vacancies, declining rentals and the threat of interest-rate hikes, many are still itching to enter the market.

We examine the case of the Tan family, which has a household income of $14,000 per month. The Tans are looking to upgrade to Bukit Timah from Sengkang as their children are studying in the top secondary schools there and they do not want them to have to endure the daily commute of more than two hours to and from school. They are considering a 1,345 sq ft, 3+1 bedroom private apartment whose owner has advertised for rent at $4,500 per month and for sale at $1.65 million.

Sell and rent in Bukit Timah

Table of Contents

If the Tans sell their Sengkang HDB flat for $450,000 and rent the private apartment for the next four years, their household expenses for accommodation would be locked in at $4,500 x 12 x 4 = $216,000.

Assuming they receive $250,000 of CPF money and another $200,000 in cash from the proceeds of the sale of the HDB flat. Over the next four years, together with their monthly CPF contributions, they would have earned 2.5% interest on their CPF balance in the Ordinary Account, or about $12,600. The $200,000 cash they received, if prudently invested, would return at least 3.0% per annum, or about $25,000 over the four years.

Overall, the rental payments and additional returns from investments would be equal to a net expense of about $178,400. On a cash basis, because the interest earned in CPF cannot be used for rental expenses, the Tans would have reduced their cash position by $191,000.

Sell and buy

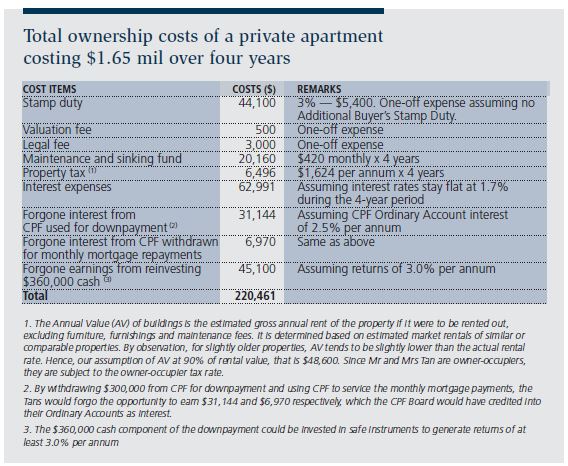

If the Tans sell their Sengkang HDB flat for about $450,000 and buy the apartment, they will need to top up $210,000 in order to pay a $660,000 downpayment, a prudent decision not to stretch their lending beyond the 60% loan-to-value ratio. Their CPF contribution would be $300,000 and their cash contribution $360,000. They will need to take a 25-year loan of $990,000 at a rate of 1.7% per annum. In this case, their costs for the next four years would be $220,461 (see table below).

Rent versus buy?

Over the four-year period from 2015 to 2019, while the total rental of the apartment is $216,000, the prudent reinvestment of the Tans’ cash from the sale of their flat could help reduce their rental expenses to $178,000. By comparison, the total ownership costs for this apartment are expected to be about $220,461.

So, it is clear in the above example that the Tans should rent. To convince them further, however, let us consider the outlook for rentals, ownership costs and home prices.

Facts and current market data

According to data from the URA, as at 2Q2015:

• 2,391 executive condominium (EC) units were vacant, representing a vacancy rate of 14.1%

• 16,626 ECs were being developed and 7,124 were launched and sold;

• 25,071 private residential units are vacant (7.9% vacancy rate), of which 22,797 are non-landed residences. The vacancy rate of non-landed residences is 9.2%. This is higher than the 7.3% in mid-2009 during the recession caused by the Lehman crisis and close to the 10% vacancy rate experienced during the four-year residential market lull between 2002 and 2005; and

• 67,211 more units of private residences will be completed in the next four years. Of these, 36,802 have been launched and sold.

Rental outlook

The total number of vacant private residential units increased 58% from 15,833 two years ago to 25,071 units in 2Q2015, but the rental index merely dropped 6% over the same period. With the strong supply expected in the public housing, EC and private residential segments, we expect rentals to be pressured downwards by as much as 30% in the next three years.

We can safely assume that the Tans will be able to reduce their rental by 12.5%, from $4,500 to $4,000 per month, when they renew their tenancy in two years. This will reduce their four-year total rental expenses by $12,000.

Outlook on ownership costs

Homeowners have enjoyed a low interest-rate environment for the last six years, and the possibility of Singapore’s home loan rates staying flat at 1.7% per annum from 2015 to 2019 is low. Assuming that interest rates rise moderately to 2.5% per annum in the third and fourth years of the Tans’ home mortgage, their interest expenses and home ownership costs will increase by $14,438.

One item that might be reduced would be property tax. After market data for rentals reflects a decrease, the annual value of properties will be reduced by the Chief Assessor. Depending on how promptly the Chief Assessor reacts to the declining market rentals, the reduction in property tax might save the Tans about $2,000 in the four-year period.

Overall home ownership costs should increase in the next few years, especially as a property ages and maintenance bills weigh in.

Price outlook — cut by scissor blades

With a supply glut building and a slowdown in employment, residential vacancy rates are expected to double by 2017 to 50,000 units. This outlook for decreasing rents should also coincide with a period of increasing interest expenses. This double whammy should cut like the blades of a pair of scissors where declining rentals meet with rising interest expenses.

If the economic outlook remains benign and current manpower and housing policies remain steady, we expect private residential prices to drop another 30% before flattening off.

In the case of the Tans, should the price of their Bukit Timah apartment fall by say 20%, their paper loss would be equivalent to $330,000 and that is as good as more than six years of rental expenses.

Conclusion

The above vacancy outlook is derived from actual construction pipeline schedules and extrapolating the past few years of demand into the future. There is no let-up on the supply once sales and construction have begun. Therefore, unless future demand can exceed the construction pace of the last eight years spurred by high population growth, any investor buying an apartment today should expect the tenant to pay lower and lower rentals in the next four years.

Many people in the industry do not like this view, preferring to stick their heads in the sand and hoping that the lifting of the cooling measures will revive investor demand. Perhaps they are correct. But the lifting of these measures will not bring sufficient tenants to fill up the expected 50,000 vacant private residences in 2017. And we have not even discussed the massive supply in Iskandar!

The case is very clear: It is better to rent than to buy — at least for the next four years.

Ku Swee Yong is a licensed real estate agent and CEO of Century 21 Singapore. He recently published his third book, Real Estate Realities — Accommodating the Investment Needs of Today’s Society. He can be reached at sku@ipa.com.sg.

Ku Swee Yong is a licensed real estate agent and CEO of Century 21 Singapore. He recently published his third book, Real Estate Realities — Accommodating the Investment Needs of Today’s Society. He can be reached at sku@ipa.com.sg.

Paul Ho is chief mortgage consultant of iCompareLoan.com. He can be reached at paul@ icompareloan.com.

Paul Ho is chief mortgage consultant of iCompareLoan.com. He can be reached at paul@ icompareloan.com.

For advice on a personal loan.

For advice on a new home loan.

For refinancing advice.

Download this article here.