“CBRE data show Singapore as the largest source of Asia Pacific outbound investment in the first half of 2018, with US$9.06 billion of capital deployed. Starved of yield and opportunities at home, Singapore real estate investment trusts (REITs) and developers have been buying overseas, especially in Australia, Southeast Asia, and Europe. In addition, Singapore acts as a through port for capital from throughout Southeast Asia and indeed globally, performing the same function that Hong Kong does for Chinese capital. The favoured destination for Singaporean

capital in the first half of 2018 was Europe, according to CBRE, with US$3.4 billion of investment.” – Emerging Trends in Real Estate® by PwC and Urban Land Institute

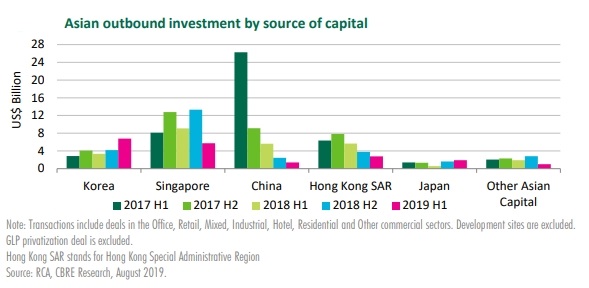

An earlier report said that Singapore is the second largest source of Asian outbound capital flows in H1 2019 after Korea despite flows dropping 37% y-o-y due to looming global economic uncertainties.

According to CBRE’s bi-annual report on Asian outbound investment released in August, Singapore now ranks after Korea as the second largest source of Asian outbound capital in H1 2019. Why Asian Outbound Investment is Here to Stay revealed that investors from Singapore spent a total of US$5.7 billion in offshore purchasing activity, while Korean investors chalked up US$6.8 billion worth of overseas transactions in the first six months of 2019.

Year-on-year, outbound capital flows from Singapore dropped 37% in H1 2019. It slid more than 50% from H2 2018, which could be seasonal since Singapore-based investors tend to be more active in the second half of the year – a trend observed since 2013.

Screengrab: CBRE

Hugh Menck, Executive Director of Capital Markets, Singapore said, “While investors from Singapore have been active in overseas investments in 2017 and 2018, the looming global economic uncertainties may have moderated their pace in general. Nonetheless, Singapore-based buyers became more active within Asia, a region that they are more familiar with, accounting for 43% of transaction volume in the region in the first half of the year.”

“In particular, Singapore-based investors have turned more active in China in the past 12 months to leverage weaker competition from domestic investors. A number of Singapore developers have made acquisitions in China’s Tier 1 cities. Given the sheer market size, China remains a major market for investors who are focused on long-term growth,” added Mr Menck.

Meanwhile, there is continued strong demand from Singapore-based buyers seeking opportunities in mature economies, particularly cities in the US and Western Europe. A select group of buyers also looked beyond the European gateway cities to Ireland and Poland.

Top five destinations favored by Singapore-based investors (H1 2019 vs H1 2018)

| No | H1 2019 | H1 20018 |

| 1 | China | United States |

| 2 | Korea | Germany |

| 3 | Japan | United Kingdom |

| 4 | United States | China |

| 5 | United Kingdom | Japan |

Source: CBRE Research

For Singapore-based investors, acquisition strategies focused primarily on structural opportunities such as logistics properties as well as defensive assets such as offices. There are also buyers who are adding multi-family assets to their portfolios. An emerging trend among Singapore-based investors is the pursuit of higher yields and alternative investments, including student accommodation and data centers.

Asian outbound investment is being spurred by new sources of capital looking for diversification

Table of Contents

In total, Asian outbound commercial real estate investment amounted to US$19 billion in H1 2019. This translates to a decline of 25% y-o-y, weighed down by the rebalancing of portfolios by mainland Chinese investors and global economic uncertainties. Despite a moderation in global capital market flows, the momentum in Asian outbound investment is being spurred by new sources of capital looking for diversification, a low interest-rate environment, historically low yields and increasing popularity in new destinations.

Dr Henry Chin, Head of Research, APAC/EMEA noted that Asian capital is not homogenous, “While there are overarching factors like geopolitical uncertainties and low interest rates which will affect the region as a whole, investors from each market possess a different set of motivations and have different options in capital deployment. For instance, low domestic yields and positive hedging environment were identified as key motivators for Korean investors’ purchasing activity, while Singapore-based investors are largely motivated by yields and are more willing to move out on the risk curve to explore alternative property investment options.”

Meanwhile, mainland Chinese investors have disposed of assets in key overseas markets including London, New York and Vancouver – albeit at significant profit – in H1 2019. This, along with existing capital controls, is likely to perpetuate the trend of net disposal by mainland Chinese investors. Purchasing is expected to be led by SWFs and corporates acquiring assets for self-use.

Tom Moffat, Head of Capital Markets, Asia said, “While the purchasing momentum by mainland Chinese investors has faded, different Asian investors will continue to seek portfolio diversification and new markets, as well as new routes into real estate, which will, to an extent, fill this gap.”

Investors from Japan re-emerge as key source of Asian outbound investment

Reemerging as a key source of capital in Asian outbound flows in H1 2019 are investors from Japan. Since the adoption of a real estate mandate by the state pension fund and subsequent foray into alternative investments, the volume of outbound investment activity by Japanese buyers increased for the third consecutive half yearly period to US$1.9 billion in H1 2019. Japanese real estate companies demonstrated ongoing demand for direct real estate investment while institutional investors still prefer indirect ways to gain overseas real estate investment exposure.

CBRE believes Asian investors can still capture alpha returns through a defensive, blended portfolio which combines both direct and indirect investments in core properties. Dr Chin concluded, “Participation in funds will be worthwhile for investors who are interested in increasing their exposure to commercial real estate, but perhaps, lack the operational expertise.”