Initial impact of Covid-19 on transactional and occupier markets around the world assessed by Savills Global Market Sentiment Survey

In its first of a series of global sentiment surveys, Savills has assessed the initial impact of Covid-19 on transactional and occupier markets around the world, with 67 per cent of countries currently reporting a moderate negative impact, and 29 per cent citing a severely negative impact.

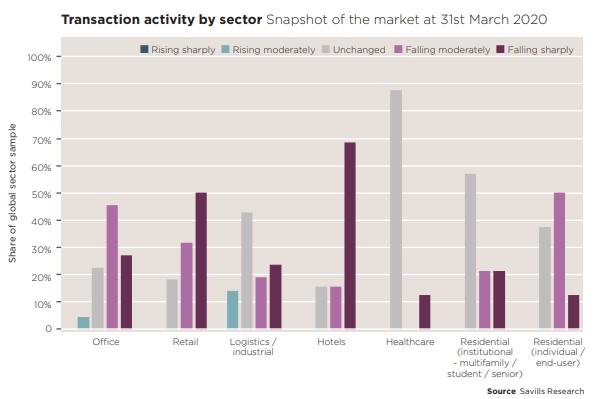

The Savills Global Market Sentiment Survey is intended to provide a snapshot of the market conditions across 24 global country markets* between 27 – 31 March 2020 based on the views of Savills head of research in each geography.

The key findings of this edition of Savills Global Market Sentiment Survey were as follows:

- Capital markets Transactional activity has been one of the most immediate casualties of the disruption caused by Covid-19. Falls in transaction volumes were reported across 62 per cent of all real estate sectors globally. The sharpest falls in activity were seen in retail, with activity reported to be down in 82 per cent of the countries surveyed, and hotels where transaction activity fell in 84 per cent of countries.

- Capital values: The impact on capital valuesis yet to be seen at the same scale, with Savills researchers seeing pricing remaining firm in 51 per cent of all sectors globally. More countries reported office, logistics and residential values as unchanged than they did falling. Retail, a sector already weakened due to structural changes prior to Covid-19, has seen falls in capital values compounded: 82 per cent of markets reported drops. Only in China, Malaysia, Vietnam and Portugal have they remained unchanged. Logistics is a bright spot, with 57 per cent of markets recording no change, or rises, in transaction activity, opposed to the 43 per cent seeing falls. Unsurprisingly, both healthcare activity and values are holding firm.

- Debt: The global debt picture is mixed. European and North American countries in particular report of tightening of availability and worse terms, most notably in the US and UK. Availability and terms remain favourable in emerging markets such as Indonesia, the Czech Republic, Taiwan and the Middle East.

- Occupier Demand: While many of companies across the globe are working from home, office space demand hasn’t been severely impacted. A moderate fall in demand was reported by 70 per cent of countries and just 13 per cent stated a sharp fall. Demand in the residential sectors has also fallen moderately. The hotel sector however has been hit hardest with 95 per cent of Savills heads of research reporting sharp falls in demand in their countries as international travel and domestic lockdowns prevent visits. Retail is in a similar situation with 74 per cent of countries seeing sharp falls. Logistics and healthcare have bucked the trend. The logistics market in particular is benefitting from increased demand from food retailers. Healthcare, unsurprisingly, is in demand at this time.

- Rental Values: The impact of this change in demand is not yet fully realised in rental values which were reported unchanged in 51 per cent of countries/sectors. The exceptions are once again retail and hotels where 30 per cent and 63 per cent of countries reported rental values to have fallen sharply, respectively. Favourable terms for retail tenants were reported in 86 per cent of countries. Just over 50 per cent of countries reported favourable terms for office tenants, and 23 per cent in the logistics sector.

Paul Tostevin, director in Savills World research team, commented on the Savills Global Market Sentiment Survey saying: “Our survey is based on the sentiment of my research colleagues around the world who are talking to a range of clients on a daily basis. They report that disruption associated with Covid-19 is having a profound impact on global real estate: overall, 67 per cent of countries report a moderate negative impact, while 29 per cent cite a severely negative impact.

“In the short term we expect to see capital values and rents follow the falls seen in transaction activity and occupier demand. COVID-19 remains a near term challenge, but certain trends, such as the shift to online retail and changing working habits may be accelerated. This could have long term implications for markets as a whole.”

Alan Cheong, Head of Research & Consultancy at Savills Singapore, commented on the Savills Global Market Sentiment Survey and added: “Singapore is no exception to what has been happening in the rest of the world. The one-month cessation of non-essential work will slow down the velocity of money owned by the masses. That will affect the consumption side of the economy. On the investment side, there is still no shortage of dry powder awaiting travel restrictions to lift so that investors to can resume due diligence work.”

“This pandemic will likely force a restructuring in the commercial and retail sectors of the real estate market here. Office tenants will think hard about the need to have all of their staff commit to full time hours in the office and spend a portion of that working from home instead. Retail may see a shift towards a higher Gross Turnover Rent percentage mode of rental collection. Industrial may return as a hot sector as last mile delivery and the need to ensure continuity in the supply chain see renewed interest by urban farmers, stockists, logistic players and manufacturers. Residential properties may also benefit as the public’s disappointment in the performance of financial assets grow and instead turn towards bricks and mortar”, he continues.