Solving Singapore’s cash problem with more cash

Table of Contents

I have been very fortunate to meet with Mr. Hari Sivan, CEO of SoCash. After learning about what his company can do, I think it has a very innovative solution that can really bring convenience to a lot of people, lower cost for Small merchants and retailers as well as bring potential extra revenue to them. People no longer have to queue at ATM machines. Banks also save money by not having too many ATM machines. This levels the playing field whereby some local banks dominate the ATM scene and became the undisputed run-away leader in deposit base, creating an unhealthy banking ecology whereby the smaller banks find it harder to compete for depositor funds and end up having higher cost of funds. Here is what soCash has to say.

By Hari Sivan, CEO of soCash

By turning ordinary stores into ATMS, soCash demonstrates how we can maintain our love for cash, while eliminating inefficiencies of the current cash flow infrastructure.

In tomorrow’s global economic ecosystem, cash may indeed be viewed by a select few as an antiquity of a bygone era.

With more businesses taking bold steps to digitise their operations, tech-based payment solutions are being developed to make the delivery of products and services between suppliers and their consumers more efficient.

But while the push towards a cashless society may seem inevitable, we must keep in mind that – for now at least – cash still reigns supreme when it comes to everyday transactions. While this is a situation more pronounced in emerging markets, many mature economies are still not totally prepared to make the full digital switch. Case in point: cash still accounts for 85 percent of transactions worldwide, with 60 percent of their value corresponding to hard cash.

At the same time, we cannot ignore the underlying reason behind why governments are trying to get more people on board the digital payments wagon: the hope for higher tax collections and expensive cash distribution networks – be it in terms of logistics or expenses – are some of the key drivers. With the economies of the world growing their incomes and, by extension, people’s spending power, the demand for cash is greater than ever before. This, in turn, means that financial systems are racing to ensure a steady supply of it.

To develop a monetary ecosystem that’s inclusive, we need to strike a balance between optimising inefficient cash networks and ensuring that cash demands can still be aptly met. As always, we look to technology to find the best answers.

![]()

Why cash is still here to stay

Thanks to the global rise in e-payment offerings, soon we won’t have to fret about whether we’ve left our wallet behind. As long as you have a smartphone, you can still pay for groceries or hail a ride without the need for holding physical cash.

At first glance, this environment may seem attractive for all stakeholders. While customers can purchase goods and services at exact amounts, digital payments mean we won’t need to carry so much change in our pockets. In this case, banks benefit too, as they get to reduce the maintenance of their highly-complex, over-engineered cash distribution networks.

Yet, as mentioned before, our propensity to use cash is still great, especially in Asia. This isn’t just considering the region’s younger markets, where we tend to attribute the importance of cash to underdeveloped financial systems and a lack of digitalisation. Even in two of Asia’s leading financial hubs, Singapore and Hong Kong, people see cash as better suited for everyday purchases like food and sundries.

While cashless solutions are becoming increasingly popular, many small businesses in Asia have shied away from implementing e-payment services as they could potentially increase business costs.

In Singapore alone, merchants – particularly those of the small and medium enterprise (SME) variety prefer using cash due to the time and financial costs involved to set up their e-payment systems. Another consideration is that implementing card payment systems means incurring transaction charges, which most merchants usually transfer on to customers through price increases. The fear of losing their price competitiveness to other smaller enterprises is often another reason for their resistance.

The challenges in applying digitisation wholescale are obvious. To illustrate: trying to pay for your transport or shopping by Paywave or Grabpay may get you some confused looks from passersby and other customers who do not have the means to do so.

But even when we look at sectors where digital solutions can be more easily applied to, there isn’t much of an uptick in e-payments either. For example, much of the trading within Southeast Asia’s burgeoning e-commerce market is being done on cash-on-delivery (COD) bases.

In considering the costs associated with going cashless, such transactions are more open to fluctuations and can drastically disrupt the world payments map. On the other hand, using cash is often free and usually requires a shorter time to settle transactions.

Optimising cash networks for the Smart City era

During last year’s National Day Rally, Singapore’s Prime Minister Lee Hsien Loong urged the country to go full-throttle in meeting its Smart Nation objectives; with the simplification and integration of payments via digital means being a key component of this plan.

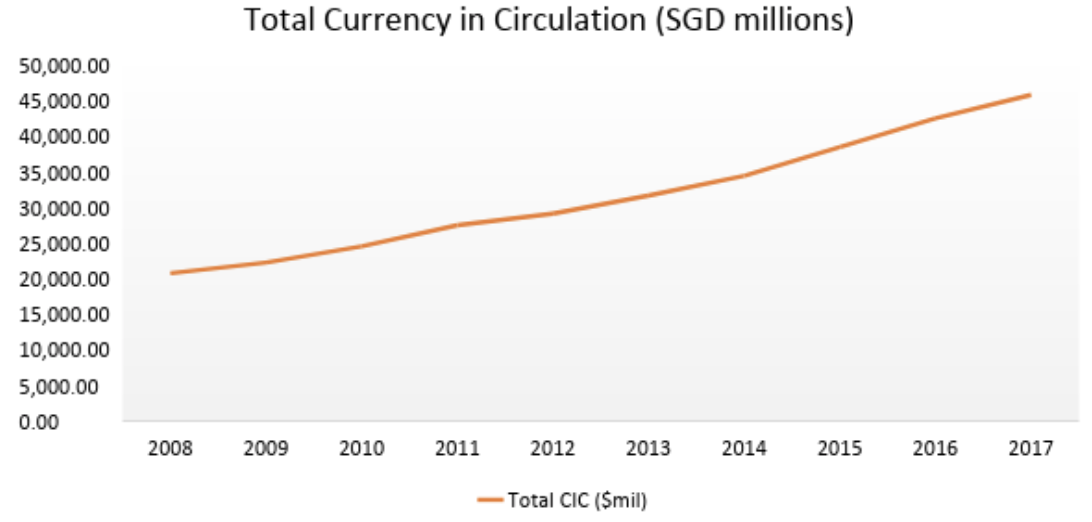

Yet, being a developed nation doesn’t mean that we are ready to wean off cash entirely. Even with the rise of cashless solutions, it should be noted that Singapore’s cash circulation is now around 8.8 percent of our national GDP – a staggering 120% increase since 2008, based on data from the Monetary Authority of Singapore (MAS).

But growing demand also means that banks need to distribute more notes. Here is where we find the crux of most governments’ arguments for developing a cashless society: to reduce our dependence on expensive ATM networks, which has grown into a massive USD300 billion industry today.

On this front, Singapore is continuing to lead innovations within the global cash logistics market. But instead of creating another solution within the cashless space, it’s allowing alternative FinTech start-ups like ourselves to bridge future and current demands of the money market.

Chart: Total cash circulation in Singapore grew by 120% in the past decade (Monetary Authority of Singapore)

How does soCash work?

soCash seeks to tap into the country’s heavy reliance on cash while making distribution networks more efficient. And we’re doing it by turning ordinary stores and minimarts into cashpoints.

A homegrown digital cash circulation platform, our app allows users to withdraw cash from stores as they would at any normal ATM. As our technology plugs directly into a bank’s API, users can place a cash order via the app and choose a nearby merchant to pick it up from. Following that, the app will deduct the selected amount from the customer’s account. This is all done digitally without the need for a card or even a PIN code.

To date, soCash has partnered with Singapore’s major banks – DBS, POSB and Standard Chartered – to provide digital cash points island-wide. This way, we’re helping to reduce operational costs for banks while making cash more easily accessible to their customers.

Reining in debt-driven consumption

Credit card debt has been one of the fastest-growing categories of consumer debt in Singapore.

This may seem strange, considering that Singaporeans tend to prefer to use cash whenever they can. In fact, a study by PayPal found that 90 percent of respondents favoured using cash and only 61 percent preferred credit cards. But when it came to using cash regularly, only 43 percent did so – alluding to problems such as having insufficient cash on hand and needing to wait in long ATM queues.

With soCash, users will have access to more cashpoints whilst shortening the waiting period to obtain cash. With the app, we also hope to help reduce people’s reliance on credit cards, lowering their credit debt. In doing so, we’re helping to promote conscious spending and encouraging consumers to spend the cash that they actually have.

Empowering our SMEs

Aside from the benefits to individual consumers, the soCash technology is also aimed at driving more business to Singapore’s SMEs, which form 99 percent of all local enterprises and contribute almost half of the national GDP. The platform taps into the country’s demand for cash and drives human traffic from ATM queues to retailers instead.

With soCash, smaller merchants can avoid rising costs while benefiting from the platform as the fees which soCash charges banks for the service are channelled electronically to these retailers. By using technology, soCash is converting cash into a commodity that Singapore’s SMEs can sell and earn revenue from.

The app also differs from conventional cashback options as it allows people to collect their money from vendors without making any purchase, which often translates into more footfall for the merchant’s business.

To date, the soCash app has integrated DBS payment APIs and DBS PayLah! as payment options for added convenience for DBS and POSB customers. With our service now available at minimarts and convenience stores island-wide – such as SPH Buzz, U Stars supermarket, iECON stores and U Mart – consumers now can use soCash as the smarter, digital alternative to queuing up at ATMs.

Still more work to do at soCash

Since launching our business in mid-2016, much our resounding success has been on the back of Singapore’s drive to continuously innovate. We wouldn’t have been able to commercially launch our product without the invaluable support of the Singapore government through its Financial Sector Technology and Innovation (FSTI) – Proof of Concept (POC) scheme; which has proven to be instrumental in our journey to improve Asia’s cash distribution network.

Singapore, however, is only the beginning of our journey to create a more efficient cash management system for the world. In Asia alone, the majority of people still value cash as their primary mode of payment.

This is because value exchange and payments remain as essential components in every economy. As our infrastructures evolve, it’s essential that we extract productivity gains on every economic activity while limiting the use of intermediaries such as card processors and payment switches, which if left without competition, can dramatically increase business costs.

Rather than fighting the tide of cashless payments, we’re working towards creating a smarter future where more people can have the luxury of accessing multiple payment options – be it cash or otherwise. While doing so, we need to ensure that such competition can drive innovation that benefits the masses; rather than concentrate pricing power in the hands of a select few.

And it’s by growing strong cash supply networks digitally where we’ll be able to democratise cash access en masse.

About the author

Hari Sivan is a former banker with more than twelve years of experience working in global financial institutions. During his time as a banker, he realised that cash circulation remained a significant challenge for many financial institutions – with uncirculated cash being locked away in ATMs which were placed in locations with low footfall – and decided to start soCash.

www.socash.io

Paul’s take on Why Small Merchants Should Sign up with soCash and why individuals should download soCash

Right now, small merchants and retailers are being saddled with huge costs of setting up Point of sales, Credit card payment terminals, Flash pay, flash this and that. Dedicated lines to connect to the network, monthly fees. Not only that, these payment methods charges a fee from 2.8% upwards on the sale to the merchants. Often, in a competitive market, the merchant may not be able to pass on the higher cost to consumers and end up incurring this cost. Personally I would really like to see the small guys win, what better ways to do so to lower cost of sales and at the same time act as a distribution channel to make some money.

And I for one hate to queue up to get cash at the ATM machines or sometimes even to drive around to locate my favourite UOB bank ATM machine.

I am so getting my soCash application downloaded. Here is the link if you want one too.

Tired of queueing up at ATMs? Use soCash instead.

Get SGD$3 for free when you sign up with this link:https://link.socash.io/UyUmnx4SAM

By the way, in case you forgot, we’re mortgage brokers and also a fellow “FinTech”, but we are not as Sexy and we cannot possibly change the world or disrupt so much as a pebble on the beach, but we are still slowly helping property agents become much more professional with helping you assess your home loan and financial advisors to help you in mortgage planning. Financial advisors and Property agents check out www.iCompareLoan.com/consultant

Do check out the latest Home Loan Rates for New Purchase or for Refinancing.

Here are some of the FinTech Problem statements defined by MAS. We do not have to work within the “problem” boundaries defined by MAS, but can go ahead and solve many problems as long as one sees a niche and a problem waiting for an answer.

https://www.icompareloan.com/resources/what-is-fintech/