Cushman & Wakefield’s 2020 Mainland China Commercial Real Estate Investor Intentions Survey report demonstrates strong investor confidence in the mainland China market, despite the Covid-19 outbreak.

Findings show strong investor confidence will cause activities to rebound within 6-months

Findings show strong investor confidence will cause activities to rebound within 6-months

The survey findings show that more than 60% of respondents believe that investment activities will rebound within six months after the Covid-19 pandemic ends, and 99% of respondents express their willingness to continue investing in mainland China.

Strong investor confidence more evident in Tier 1 cities

In terms of investment in cities, investors are more enthusiastic about Tier 1 cities, especially foreign investors, with 100% of respondents from foreign institutions stating they have plans to invest in Shanghai in the next 12 months. Despite the impact of the pandemic, most investors have confidence in the market and are optimistic about the long-term development of the commercial real estate (CRE) market in mainland China.

Strong investor confidence reflected in one-to-one interviews

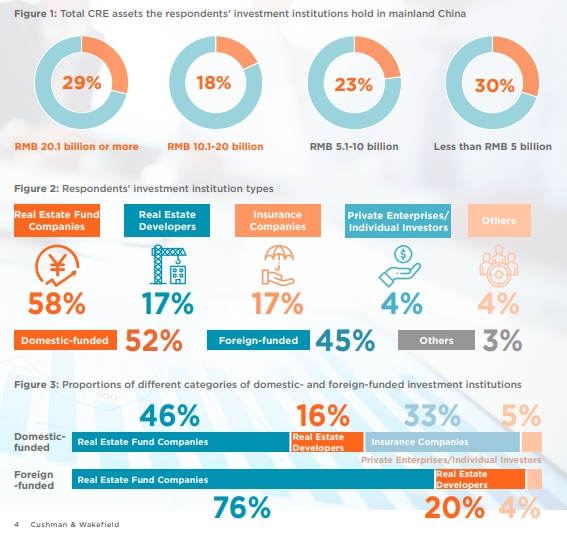

The survey took the form of one-to-one interviews, with senior management of the most active investment institutions in mainland China over the last three years invited to participate. The project accumulated 122 valid survey completions and analyzed them to provide investors with timely market intelligence.

James Shepherd, Head of Research, Asia Pacific at Cushman & Wakefield, said: “The survey results show that domestic investors are more proactive than foreign investors in terms of project execution, and more willing to increase their investment budget in 2020. Impacted by the Covid-19 outbreak, most foreign-funded enterprises have significantly slowed their project progress, which provides domestic-funded enterprises with opportunities to accelerate their pace of acquisition.”

Alvin Yip, President of Capital Markets in Greater China, and Head of Capital Markets in China at Cushman & Wakefield, mentioned: “Looking back at past crises, the impact of SARS in 2003 was not prolonged, as China’s economy was in a period of rapid growth, and although the global financial crisis of 2008 took a toll on the global economy, China’s real estate market rebounded rapidly afterwards due to high liquidity in real estate projects and a healthy financial market.”

“Today, most investors have become accustomed to turbulence. The straight rise in asset values over the past few years has kept investors waiting for new market entry opportunities should a correction arise. With the China government’s concerted effort to control the coronavirus, and with the support of economic stimulus measures, we are hopeful that its impact will only be short-term. Experienced investors may find this an opportunity to expand their footprint in China,” Yip added.

Catherine Chen, Director of Research, Asia Pacific at Cushman & Wakefield and author of the report, commented:“We can see from the findings of this survey that investors generally have an objective view on the impact of Covid-19. They believe that the pandemic will have certain negative impacts on the market in the short-term, especially in the office, retail and hotel sectors, but this short-term impact will not cause them to abandon their investment.”

“Under the impact of the pandemic some industries are experiencing rapid growth in demand, such as online retail and services, artificial intelligence and big health. We anticipate that this growth will lead to the further development of the CRE sectors supporting these industries, including data centers, logistics and R&D centers.”

Shepherd added, “For investors who are based in Asia, China is an important part of their portfolio allocation in the Asia-Pacific region. We expect that there will be a range of investment opportunities in the market when the pandemic situation gradually becomes clearer, and transaction volume may rebound in the second half of the year.”

Strong investor confidence in alternative assets

A recent report by CBRE said that although mainland Chinese investors’ capital outlay slowed for the second consecutive year, some investors from this market have shown a proclivity for alternative assets, such as senior housing, a notable transaction being Cindat Capital’s acquisition of a UK-based portfolio in H2 2019, adding to its 2017 acquisition of a senior housing portfolio in U.S.. Asset disposals by investors from Mainland China continued in 2019; however, the rate of disposal was lower than the amount recorded in 2018.

Dr. Henry Chin, CBRE’s Head of Research, APAC/EMEA, said, “Investors from Hong Kong and Singapore are expected to continue paying close attention to European markets throughout 2020. The easing of geopolitical uncertainties post-Brexit are also expected to reignite investors’ interest in London in 2020.”

“In 2020, we expect commercial real estate investors in Asia Pacific to continue seeking higher returns and portfolio diversification opportunities outside of their domestic markets. As the upward market cycle reaches maturity, it is projected that investors in the region will turn to assets with stable income streams,” he added.

The report by CBRE, Asian Outbound Investment 2019, said for the second consecutive year, Singapore topped Asian outbound real estate investment in 2019 at US$15 billion, albeit reflecting a 33% decline y-o-y from the US$22 billion registered in 2018. Meanwhile, Asian outbound commercial real estate investment fell 17% y-o-y to US$45 billion in 2019. The perpetuation of capital controls in Mainland China was the primary reason for the moderation in overall investment activity across the region.

Mr Michael Tay, CBRE’s Head of Capital Markets, Singapore said, “For Singapore, the 33% y-o-y decline in investment volume was due to the lack of large portfolio transactions recorded in 2019. This is compared to 2018, during which Mapletree Investments acquired two overseas logistics portfolio that amounted to US$4.2 billion. While office assets have been typically favored by Singapore-based investors, it is observed that in 2019, there had been stronger interest among a select number of Singapore investors shifting to look for income-generating assets in alternative sectors such as student housing.”

Top 3 asset types favored by Singapore-based investors (2019 vs 2018)

| No. | 2019 | 2018 |

| 1 | Office (US$9 billion) | Industrial and Logistics (US$8 billion) |

| 2 | Industrial and Logistics (US$1.4 billion) | Office (US$7 billion) |

| 3 | Residential including student housing and multi-family (US$1.3 billion) | Mixed-use projects (US$4 billion) |

Source: CBRE Research