The Pricing Impact of a Change in Down-payment Percentage for Housing Loans

By PEARL LIM

From an economic perspective, any change in credit conditions will have an impact on demand thus bringing about a change in market-clearing price and (or) sales volume. Down-payment forms an essential component in the financing of a property purchase. In the Singapore’s context, for residential property purchases, down-payment is funded by cash and (or) Central Provident Fund balances. This implies that a raise in down-payment as a percentage of the purchase price [equivalent to a lower loan-to-value ratio (LVR)] will lead to, ceteris paribus, a decrease in demand for residential property. Intuitively, the decreased demand is spurred by the greater number of buyers exiting the market. Generally, for first-time buyers accumulating the savings needed for down-payment constitute a major hurdle in property purchases hence a lower LVR will deter this group of buyers from making purchases. Repeat buyers who wish to upgrade or purchase another property will be hesitant to do so thus depressing demand.

A Look at the Effect of a Change in Down-payment Percentage

Table of Contents

Using a simple demand-and-supply analysis, we will illustrate the dynamics of an increase in the down-payment percentage. We assume the classic case of a downward-sloping demand curve and an upward-sloping supply curve. On the supply side,the key determinant of the magnitude of change in market-clearing price and sales volume is the price elasticity of supply. This parameter measures the relative responsiveness of quantity supplied due to a change in the price of the good itself, ceteris paribus.

For simplicity, we omit the two extreme cases of a perfectly price elastic supply (PES= infinity) and a perfectly price inelastic supply (PES=0).

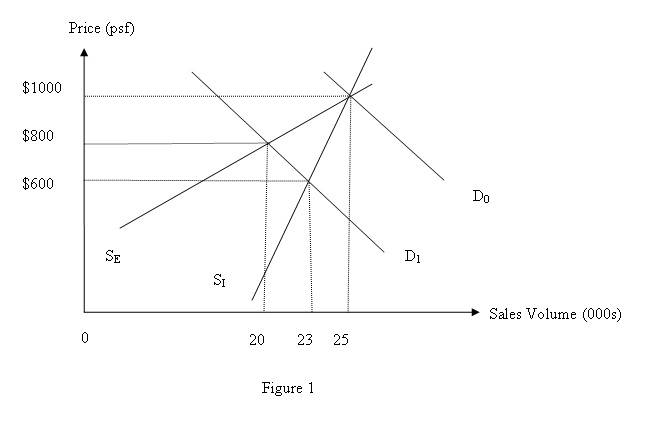

SI is the supply curve that is relatively price inelastic (PES < 1)

SE is the supply curve that isrelatively price elastic (PES > 1)

Figure 1 shows that when down-payment rises, ceteris paribus

i) the demand curve for property shifts to the left from D0 to D1

ii) there is a decrease from the initial market-clearing price of $1000 psf and sales volume of 25000

iii) the magnitude of decrease in market-clearing price and sales volume is contingent on the price elasticity of supply

iv) when the supply curve is relatively price elastic, SE,the market-clearing price and sales volume decrease to $800and 20000, respectively.

v) when the supply curve is relatively price inelastic, SI,the market-clearing price and sales volume fall to $600 and 23000, respectively.

Hence we can conclude that if supply is relatively price inelastic, the decrease inmarket-clearing price is steeper, but the fall in sales volume will be smaller.

In the short run, it is realistic to believe that the supply of housing is relatively price inelastic as property developers cannot quickly adjust supply in response to demand changes. For example, developers are unlikely to put off property launches that have been planned before the fall in demand.

In contrast, in the long run, developers can reduce the construction of new property; consequently supply becomes more elastic.

In the Singapore’s Market Context

Relating this economic analysis to the Singapore’s residential property market, we do observe the Government implementing cooling measures aimed at increasing the down-payment percentage. Since Sept 2009, the Government has made six legislative attempts to stabilise soaring property prices, with the latest, on 6 October 2012, being the further decrease of the Loan-To-Value ratio (LTV) for longer term loan. (With the new regulation and the weak economic climate, you will want to optimise your financial resources when applying for new home loans or refinancing your current one. Do make use of the free mortgage advisory service at www.iCompareLoan.com to find the best home loan in town that will serve your needs.) Among the slew of measures, four specifically target an increase in the down-payment component.

Chart 1: Cooling Measures that Affect the Down-payment

|

Date |

Policy Change |

| 19 Feb 2010 | Lowering of Loan-To-Value ratio (LTV) from 90% to 80%. |

| 30 Aug 2010 | Increase in Minimum Cash Deposits from 5% to 10% and a Decrease in Loan-To-Value ratio (LVR) to 70% for Property Buyers with Outstanding Housing Loans. |

| 14 Jan 2011 | Further Lowering of Loan-To-Value ratio (LVR) to 60% for Property Buyers with Outstanding Housing Loans.For Non-Individuals Borrowers, Lowering of Loan-To-Value ratio (LVR) to 50%. |

| 6th Oct 2012 | For Loans Exceeding 30 Years or Which Extend Past the Age of 651) Further Lowering of Loan-To-Value ratio (LVR) to 60% for Property Buyers Taking their First Housing Loans.2) Further Lowering of Loan-To-Value ratio (LVR) to 40% for Property Buyers with Outstanding Housing Loans.For Non-Individuals Borrowers, Further Lowering of Loan-To-Value ratio (LVR) to 40%. |

Source: CPF, Singapore SIBOR Watch, The Straits Times

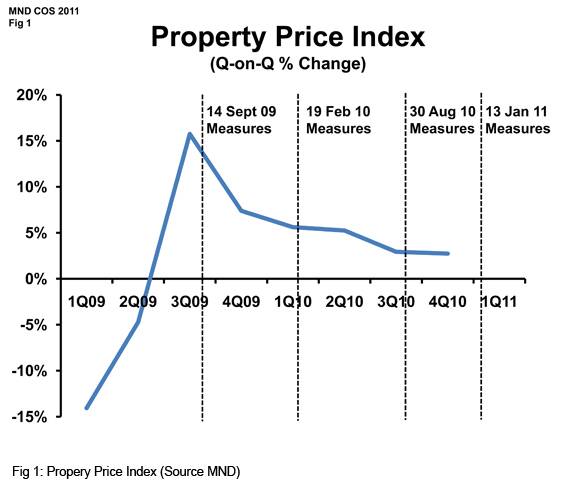

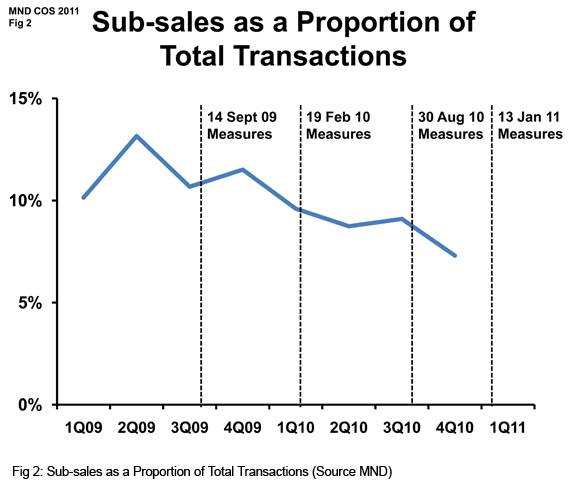

Based on then Minister of National Development, Mr Mah Bow Tan, in the Committee of Supply Debate speech delivered on 3 March 2011, the four rounds of cooling measures have proven effective in reining in prices. (See below two figures)

“Resale price growth and transaction volumes have moderated. Quarter-on-Quarter growth in resale prices slowed from 4.0% in the second and third quarters of 2010 to 2.5 per cent in the last quarter. For 2011, month-on-month, resale price growth has slowed to 0.6 per cent in Jan and 0.7 per cent in Feb. The trend is still downwards. Likewise, quarterly resale volumes fell by 21 per cent to about 6,500 transactions in the last quarter of 2010, or about 2,200 transactions each month,” Mr Mah said.

In addition, according to Ku Swee Yong, CEO of International Property Advisor Pte Ltd, in his evaluation of the first four rounds of cooling measures commented that the “The tightening of the loan-to-value (LTV) ratio from 70 per cent to 60 per cent had the largest impact on market volume” (page 37).

To counter the series of stringent measures, property developers have come up with various cashback schemes to woo buyers. Among which includes dishing out furniture vouchers and early birds discounts.

For advice on a new home loan.

For refinancing advice.

Download this article here.

References

Ku Swee Yong, Real Estate Riches: Understanding Singapore’s Property Market in a Volatile Economy, Singapore: Marshall Cavendish Business, 2011, 37, Print

“35-year Limit Set on Home Loans”, The Straits Times 6 Oct 2012, sec 1: 1, Print

“my CPF – Buying a House. . . A Place to Call Your Own”, Central Provident Fund Board, Web

<http://mycpf.cpf.gov.sg/CPF/my-cpf/buy-house/BH5.htm>

“Summary of Property Cooling Measures”, Singapore SIBOR Watch, Web

<http://singaporesiborwatch.com/singaporesibor-learning-centre/summary-of-property-cooling-measures-imposed-by-the-singapore-government/>

Speech by Minister for National Development, Mr Mah Bow Tan, at the Committee of Supply Debate on “Stability – Responding to extraordinary growth”, 3 March 2011, Web

<http://app.mnd.gov.sg/Newsroom/NewsPage.aspx?ID=2381&category=Parliamentary%20Speech&year=2011&RA1=&RA2=&RA3=>

Images/Charts for Speech by Minister for National Development, Mr Mah Bow Tan, at the Committee of Supply Debate on “Stability – Responding to extraordinary growth”, 3 March 2011, Web

<http://www.mnd.gov.sg/BudgetDebate/bavr2011-photo01.html>