Types of Loans in Singapore and its different Financing Costs

Table of Contents

Individuals and businesses alike, do you know what is the cheapest form of financing and whether there are any conditions attached to it?

Let’s face it, not all loans are created equal. Why are some loan interest rates higher and why are some lower? This is because some borrowers are less risky than the others whilst some are highly risky and can take the money and run, therefore the different interest cost merely reflects the different risks incurred by the lender.

What are the types of loans in Singapore? Which are the cheapest form of financing and interest rates in the world? How to make the correct decisions about how much to pay for a loan?

| Types of Loans | Effective Annual

Interest Rates % (~in 2018) |

Tenure or Duration |

| Residential Home Loan | 1.6 to 2.6 | Up to age 65 or 75 |

| Commercial & Industrial Property Loan | 2 to 3.5 | Up to age 70 generally |

| Car Loans Personal name | 4.5 to 6.5 | Up to 7 years |

| Car Loans Company name | 5.5 to 9 | Up to 8 to 10 years. |

| SME Micro Loan | 6 to 8.75 | Term 1 to 3 years |

| SME Loan – Secured with Property | 6 to 12 | From 1 to 5 years |

| SME Working Capital Loan up to $300,000 | 6.5 to 8.5 | From 1 to 5 years |

| Unsecured Business Term Loan (Working Capital Loan) | 8 to 15 | From 1 to 5 years |

| Pawn shop | 10 to 12 | 1 month to 12 months |

| Personal Loan Banks | 9 to 18 | From 1 to 5 years |

| Peer-to-peer corporate lending | 12 to 20 | 12 months typical, up to 5 years. |

| Factoring and Invoice Discounting | 20 to 40 | 60 to 180 days (typical) |

| Credit Cards | 19 to 29 | Daily Rest (Monthly roll-over) |

| Money Lender | 30 to 48 | 1 month to 6 months typical |

| Business Bridging Loan | 40 to 75 | 1 month to 3 months |

Table 1: Types of Loans in Singapore and its estimated interest costs in 2018, iCompareLoan.com

We leave out Renovation loan as the approved amount is only very tiny and we also leave out education loan as it is of a different nature.

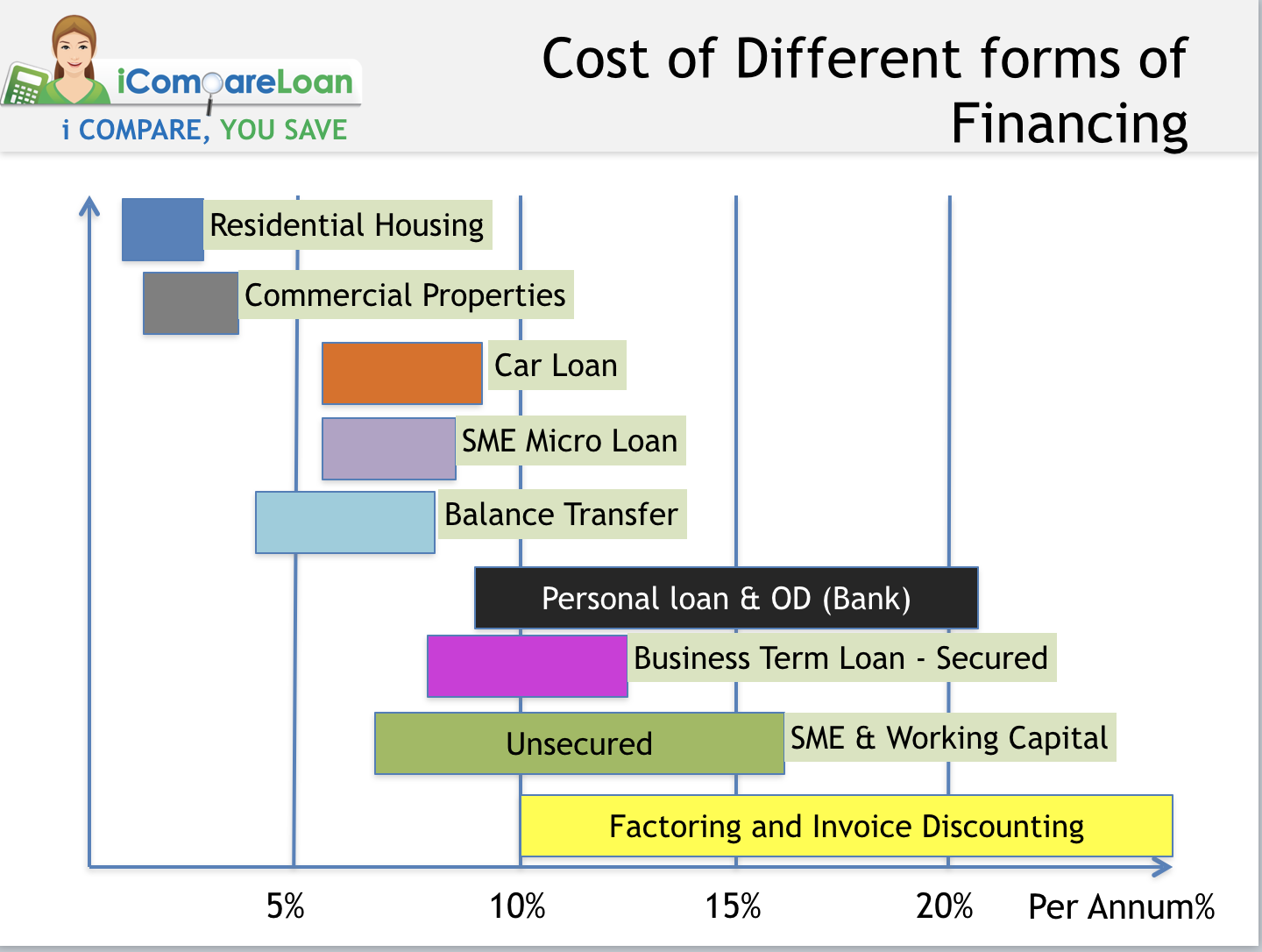

What are the types of loans available in Singapore? Here is a snapshot of some of the main ones.

What are the types of loans available in Singapore? Here is a snapshot of some of the main ones.

Image Credits: Common types of loans available in Singapore and its estimated financing costs, Presentation slides at a joint event with Credit Bureau Singapore, iCompareLoan

Cheapest types of Loans in Singapore – Your Parent’s loans

Parent’s loans are typically the best. Parent’s generally make very bad bankers, they cannot count and they are bad credit assessment officers. Often they give out personal loans at zero interest rate and with no stated repayment time-frame and there is no enforcement for non-payment and of course, no IOU.

Verdict: 0% Interest Rate with No time-frame for repayment and no enforcement ability.

Secured lending are all those loans that are backed by assets and will be cheaper compared to those that are unsecured and backed only be reputation, etc.

Here is a snapshot of the different types of financial options and their financing costs: –

Residential Home Loans

The next cheapest loan comes in the form of residential home loans. This is because in Singapore, a home is valued at $1 million, a loan of only $750,000 (July 2018) is lent out. Even if a borrower defaults on the payment, it is easy to let go of this property for $950,000 or thereabouts, this means that the lender is practically assured of their capital. Currently most banks do not price home loans for own use and investment use differently. If banks ever price their housing loans differently, I would expect the housing loans for investment will be more expensive that those for owner occupied units.

Housing Loan rates: Ranges from 1.8% to 2.6% (Based on Oct 2018).

Read more about the best home loans in Singapore here.

Commercial and Industrial Property Loans (CIP Loans)

CIP loans or commonly referred to as commercial property loans by the layman generally refers to loans for Retail, Offices and Industrial properties. These loans are backed up by the properties as assets.

Retail: Shops in shopping centres, shophouses, HDB shophouses, Conservation shophouses.

Offices: Office units within a building, they are usually located on the higher floors and have no frontage. Some offices are located on the second and third floor of shophouses whilst some are offices that combines with retail.

Industrial: Industrial properties generally have 2 types. B1 and B2. B1 refers to light industrial units where light and low pollution industries are allowed to participate and locate, while the B2 are those deemed to be heavy industry with higher level of pollution, such as noise, dust, chemical or hazardous substance, dangerous and large machinery, etc. There are HDB industrial properties, JTC industrial properties. Those who are JTC industrial properties are often B2 category.

Therefore banks may offer different rates for different structures, such as

; –

- Personal names

- Investment holding companies

- Operating Companies

Interest Rate range: 1.7% to 3.5%

And those that are used for own use are approved for higher loan amounts and potentially cheaper rates while those that are for investments are offered lower loan amounts and often slightly higher rates due to the risk of renting them out and therefore the ability to repay the loan.

Bank’s core business is in loans and interest income they are not here to take your property.

Car Loans in Singapore

Car loans are also secured loans. They are secured by the vehicles, and is also considered safe for the banks. Hence their interest rates are also low.

Car loans are typically sorted into the following categories for Passenger Cars (namely those that are saloon or SUV): –

- New car loans – Personal name

- Used car loans (less than 10 years) – Personal name

- Used car loans (more than 10 years) – COE Loan – Personal name

- New car loans – Company name (Director own use)

- Used car loans – Company name (Director own use)

- New car loans – Private Hire or Limousine Services company (Director use + Staff use) – The staff or associates are the Grab, Uber, Ryde or other car hailing app users.

- Used car loans – Private Hire or Limousine Service Company (Director use + Staff use) – The staff or associates are the Grab, Uber, Ryde or other car hailing app users.

- New Car Loans – Private Hire or Leasing Company (This classification can be rented out to individuals or companies for passenger self drive, but cannot be used for ferrying people for a fee)

- Used Car Loans – Private Hire or Leasing Company (This classification can be rented out to individuals or companies for passenger self drive, but cannot be used for ferrying people for a fee)

Commercial vehicle loans will be more complex and incur higher interest costs. The loans may be from a bank or a credit company. Many credit company also hold moneylending license and they lend out money for vehicle loans or short term bridging loans. Commercial vehicle loans are more expensive than passenger car loans.

- Vans and Goods vehicles or lorries – under company name

- Other commercial vehicle – under company name (More exotic)

It is worth it to note, credit companies play an important role in Bank’s Car Loan paperwork processing.

Car Loan Interest Rates: 2 to 4% Flat (or 4 to 9% effective Interest rates)

SME Micro Loan up to S$100,000

There is much talk about SME Micro loan, but to qualify, companies need to meet certain criteria set. Registered and operating in Singapore, 2 years preferred, at least 30% local shareholding, Annual sales of up to S$1 million or up to 10 employees. The scope is however for daily operations and for you to automate and upgrade factory. Most companies who apply do not get $100,000, many who are lucky end up with $20,000 to $30,000.

Interest Rate Ranges: 3.2 to 4.7% (~Effective 6% to 8.75%)

SME Loan – Secured with Property

Often you run a small company, you have already maxed out your company loan. Perhaps this year, your company is not profitable, you need some funds to tide you through the rough patch.

You may consider equity-term-loan from your current residential property if you have sufficient income. Often entrepreneurs do not declare sufficient income and moreover self employed income is treated with a 30% haircut which makes passing TDSR harder.

If you have a paid up property or a property that has very little outstanding loan, you can pledge your property to the bank/financial institution or corporate lenders who can consider lending you money for your business expansion.

Interest Rate ranges: 6% to 12% + Admin fees + Legal Fees + valuation and Processing fees. (Loan brokers typically charge 2 to 5% to help you manage this process)

SME Working Capital Loan – up to $300,000

The SME Working Capital Loan is a government assisted financing scheme from Spring Singapore. The government co-share possible default risks with banks, so that banks are more willing to lend to businesses. This is available till May 2019. You cannot simply come in and ask for $300,000 and get it, it depends on your profitability, cash flow and credit status.

Interest Rate Ranges: 6.5% to 8.5% Effective Annual rate.

Unsecured Business Term Loan (Working Capital Loan)

For companies that has already tapped into cheaper source of funding such as SME Working capital loan and still need more funding, they can use unsecured business term loan for expansion. Some companies that are bigger may not qualify for SME working capital loan may also use unsecured business term loan. Do note that the range varies widely depending on the credit quality of the company.

Interest Rate Ranges: 8% to 15% Effective annual rate

Pawn Shops – Secured Lending

This is the most traditional form of lender. You can bring in your Rolex or Gold Chain or precious jewelry for a loan.

Interest Rate Ranges: 10 to 12% Effective Annual rate

Personal Loan Banks – Unsecured

Personal loans are also a good source of temporary funding for small business owners. The interest rates ranges widely. However the maximum unsecured loan a person can borrow is 12 times their monthly income coming Jan 2019. You can only tap into personal loan if you earn more than $30,000 a year (Singaporean) or $60,000 for (Singapore PR or EP). Not everyone qualifies for personal loans from the banks.

Interest Rate Ranges: 9% to 18% Effective annual rate.

Peer-to-peer funding or Alternative Corporate Lending

These platforms typically takes time to garner up enough funds. And speed of raising the debt is usually quite slow. Moreover, the nature of this tends to be more public, while some say this also acts as a form of branding to raise the profile of the borrower, some businesses may not feel that way.

Interest Rate Ranges: 12% to 20% Effective annual rate.

Factoring and Invoice Discounting

Banks provide factoring and corporate funders provide invoice discount in which they will fund you for the goods and services that you sold to a reputable buyer. Businesses need this sort of funding when the companies they supply to tend to pay slowly or have long credit terms. In some industries, delaying payment is an industry practice. Let’s say you sold $100,000 worth of goods (your cost is $70,000 and you make $30,000), but the buyer does not pay you till 180 days later. So in order for you to capture the next batch of deal, you will need to first cough out another $70,000 cost of goods and then to sell it for $100,000. You can then sell your $100,000 invoice to the bank at a discount of maybe $95,000, and you get your money upfront so that you can go and make more money. Some form of pledging or director’s guarantee is usually required.

Recourse Method

The bank lends you the money first, but in case the buyer defaults on paying, you are still liable. This is called the recourse method.

Non Recourse Method

There is also another method whereby the bank/funder simply buy out your invoice at a discount and they bear the default risks, this is called the “Non Recourse method”. This is more costly and is usually on a per transaction basis. This could cost up to 8% per transaction.

Interest Rate Range: 1.5% to 3.5% per month up to 180 days, some are charged based on 5 to 8% per transaction, hence could end up as 20% to 40% per annum or even more.

Business Bridging Loan

Business could need funds from time to time, such as bidding for a project and needs a project deposit, emergency payments to suppliers or to participate in an investment. These funding are needed very quickly and the sums are big. These kind of loans are typically provided by credit companies or alternative corporate funders. As companies typically may not have sufficient revenues or may not be hugely profitable to qualify for the huge funds and different types of loans in Singapore are explored and exhausted, therefore the individual’s assets could be used as a second charge.

Interest rate range: 3 to 6% per month up to 6 months, 40% to 75% a year. Legal fees are typically paid by borrower, SME loan consultants charge 3 to 5% for structuring such loans.

Credit Companies and Money Lender

Credit companies and money lender serves a function in the society. You can go to a legal money lender if you fail the credit assessment or if you do not meet other income eligibility criteria. As the risk of you not paying up the loan is higher and there is no security, the interest rate is higher to compensate for that.

Interest Rate Range: 3 to 4% per month (max 4%) or around 48% per annum with Admin fee up to 10%.

Read more about personal finance here.