What is Fintech? Can it change the Property and Finance Segment

FinTech is loosely defined as the technology that can solve Financial industry’s problems. PropTech is loosely defined as the technology that can solve Property Industry’s problems. Each industry has its own inefficiencies and pain points and is defined by the “Problem statements”. For example, MAS has created 100 problem statements within the Financial Sector, these are the problems or issues that the industry face day-in day-out.

What is FinTech? Who defines FinTech?

Table of Contents

FinTech, PropTech, LegalTech, logisticsTech and so on, a lot of new terminology invented. Startups are rushing to call themselves the latest names.

China leads the world in FinTech. In China, many people do not carry cash anymore, even insurance can be bought on your mobile phone via AliPay or ANT Financial or WeChat Hong Bao.

While China is the world leader in FinTech, WeChat and Alibaba (Alipay) grew despite of the government, rather than because of the government.

What problems does FinTech Solve?

To qualify as FinTech, a company must be able to do the following for the financial industry: –

- Faster

- More accurate

- Safer (such as crytography and security)

- Cheaper (lesser administrative chores)

- Provide greater convenience (such as mobility)

- More transparent

- Consolidate and aggregate across many different platforms

Most technology companies do not make money for many years. They are in it to change the way the world does things. Apart from a few stellar high profile examples, such as Google, Facebook, Linkedin, Alibaba, Paypal, Tencent, Baidu, very few make money in the short term. Even Amazon took more than 20 years and has very little profit to show, despite its dominance in online shopping.

Monetary Authority of Singapore (MAS) hosted a FinTech Hackathon (Hackcelerator) on 15th Aug 2016 where they invited people from all over the world to attempt to solve problems relating to the Financial industry. MAS has also created, in my opinion one of the best FinTech Problem statements ever created by any government statutory board or central bank. This serves as a map or reference for technology companies to navigate. MAS did not mention peer-to-peer financing or cryptocurrency which in my opinion are also interesting areas that can bring capital to segments where banks may not be interested in (based on today’s traditional underwriting rules).

Infographic 1: Visible Segments within the Financial Sector where FinTech problem statements can solve, iCompareLoan.com

Infographic 2: Back-end and not so visible to the public problem statements in the Financial sector, iCompareLoan.com

What is a problem statement in FinTech?

MAS highlighted 100 problem statements, they are the issues faced by the financial industry today.

Areas identified are: –

Know Your Customer (KYC) /Identity Authentication – 7 Problem Statements

- 7 problem statements which includes document document, Authentication methods, common platform, secured transmission, central platform, secured platform and central repository.

You will not get to hear much about these areas unless you are as nerdy as I am. How to make sure of the authenticity and identity of the person signing the documents. This is a problem area created by onerous regulatory oversight on the Financial industry.

RegTech – 8 Problem Statements

- 8 Problem statements about compliance and regulatory technology.

This relates mainly to supervisory controls on the financial markets, compliance, transaction controls, etc. This is segment for the big companies, usually reserved for those who are 100 million or above in capital.

Trade Finance – 4 Problem Statements

- Addressing the Lack of awareness of trade and credit products, multilaterally verified Contracts, Difficulty in digital supply chain financing.

These problems are potentially solved by Blockchain technology, Smart Contract, digital documents and common platform and repository to verify contracts.

Crowd funding companies with credit scoring, underwriting abilities such as Moolahsense, CoAssets, Ricco Capital (provisional license) and Invoice Interchange, Fundplaces fill the gap in property development financing.

However one major headache is the need to obtain a capital markets license, increasing the cost and paperwork.

There are also gaps in peer-to-peer lending as consumers cannot get access to cheap emergency funds and often having to resort to loan shark. However this segment cannot develop in Singapore as lending to inviduals is governed by the money lender act.

Insurance – 14 Problem Statements

- Problems relating to Insurance claims processing to pricing of insurance products to Contracts and underwriting.

This is a boring area relating to the insurance back-end such as claims processing and mainly dynamic underwriting leveraging data and medical records. There are a lot of inefficiencies in the insurance industry that is not about to be solved anytime soon.

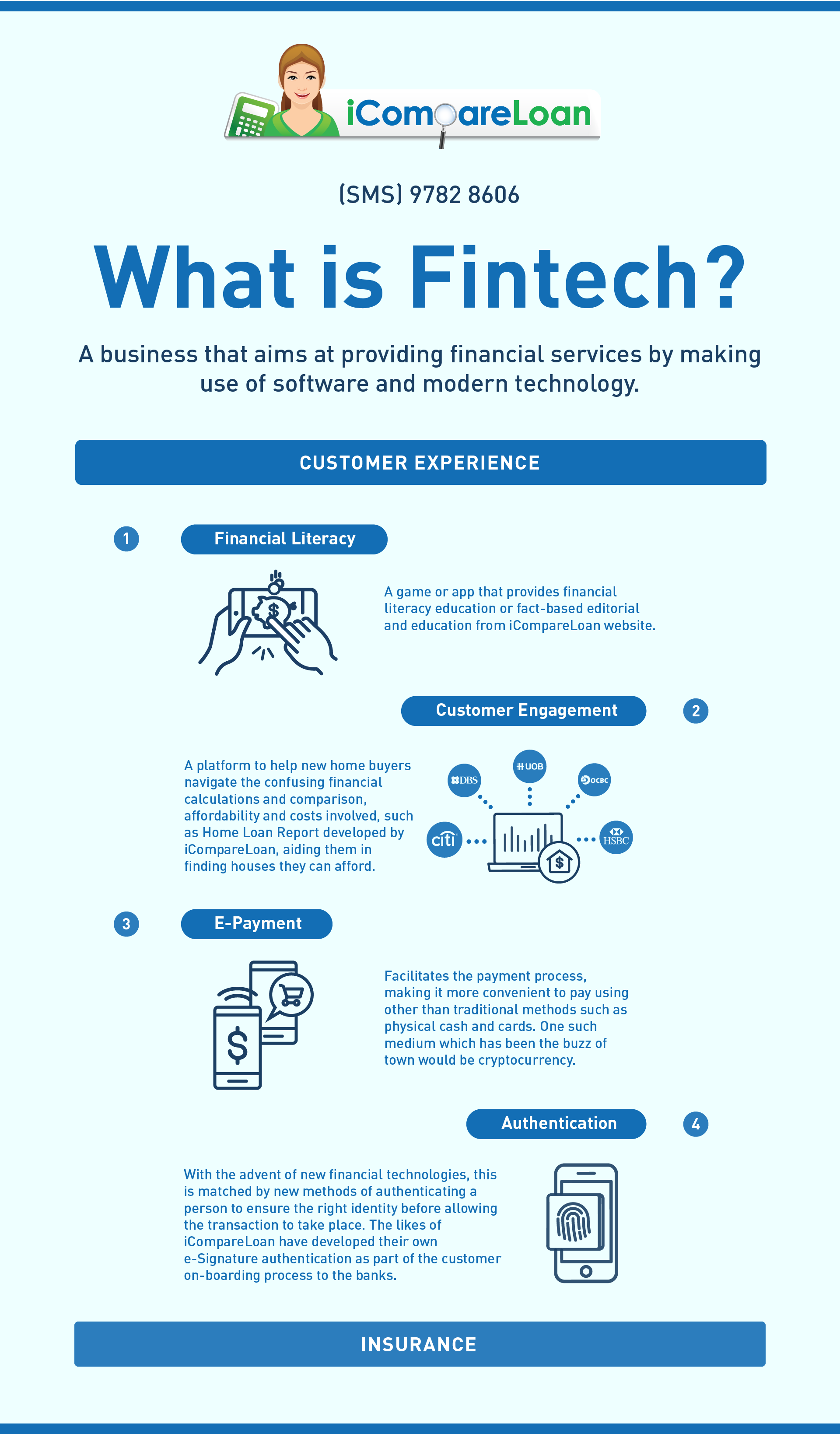

Financial Literacy – 5 Problem Statements

- Problems on Financial literacy in Personal finance management, Gamified Investment Tool, Financial Education tool and Financial Education Application.

This area covers customer education and making financial education fun. Assist consumers in making holistic plan for themselves by personal finance management.

Financial Inclusion/SMEs – 10 Problem Statements

- Problems relating to inclusion of unbanked customers, micro-services, finance & accounting suite that can include smaller companies, credit underwriting and evaluation, mobile payment and administering aid.

This is an area where mobile payment, e-wallet can help. Automating Finance and accounting for SMEs making sure that they can also scale the big league. Most SMEs today still face high fixed cost overheads due to their smaller scale.

Crowd funding can also assist the bank in serving SMEs with lower credit rating.

Customer Engagement – 12 problem statements

- Aggregated News for Investment

- Financial Data Analysis

- Financial Analysis for Home Buyers

- Aggregated Loyalty Rewards

- Customised Loyalty Rewards

- Aggregated Financial Statements

- Mobile Banking for the Visually Impaired

- Aggregated Personal finance

- Aggregated Savings Platform

- Customer Data analytics tool

- Mobile Tax Refund

- Innovative Digital Banking

Payment – 11 Problem Statements

- Problems relating to enabling Seamless Payment Solution, Internet of Things (IoT) by integrating sensors, actuators, computing capability to devices within Financial services for better Financial decision making, digital cheques, API gateway for connectivity to different payment platforms, efficient settlement, cashless schools, payment for low-value trasaction, seamless season parking fee payments, enhanced mobile wallet, automated payment engine, cross-platform payments.

This is the most sought after area where industry titans and small players alike entered. Industry giants such as Paypal, Alipay, WeChat Pay and QQ Pay and many more.

Portfolio Management – 12 problem statements identified.

- Automated institutional investments, Predictive FX Rate Model, Real-time diagnostics to detect wrong NAV calculations, Interactive customer evaluation to assess customer’s risk profile, smart portfolio management that builds in decision making factors to construct customer’s portfolio, Real-time investment advice with Robo-advisors, Data driven investment recommendations, neutral platform for structured products, investment management tool, Robo-advisor, straight-through processing of orders, research aggregation service, automated reporting. These are the costly paperwork and inefficiencies causing the portfolio and fund management industry to stagnate.

This relates to funds and fund management, so is not so interesting for many people. You will not hear much about this segment as a consumer.

Capital Markets – 7 Problem Statements

- Problems centres around efficient payment settlement, transaction and trade settlement, secure distributed platform for interest rates, transparent distribution pricing, integrated FX marketplace and Collateral & Risk management.

This is also for the capital markets and transaction and trade settlement within the capital markets, such as stock exchange and other exchanges.

General – 9 Problem statements

- Problems relating to tailored training, automated training, automated operational performance reports (Dashboards), compliance testing, automated translation, automated reports formating, layered data encryption (for cybersecurity), unique transaction identification recognised for OTC and online and safe data sharing.

What do some Consumer facing FinTech companies do?

CardUp

Allows users to use credit card to make payment on rent, MCST fees and bigger ticket regular payments in return to earn airmiles. They tie up with credit cards to offer benefits to consumer. They are not really disruptive but does nonetheless solve some needs identified in MAS’ top 100 problem statements, in the Customer Engagement space in FinTech to consolidate consumer’s spending into 1 place. Potentially this company also has ambitions in the eWallet space to address needs in the Payment space.

There are many such start-ups and they aim to capture a big slice of the big ticket items “payment” transaction flow and in return, they capture a percentage of the payment flowing through.

GrabPay

Grab started as a Ride hailing application, taking a cut from matching driver with consumer. Definitely not FinTech to start off with. Of late, Grab indicated that their intention and focus is on developing a payment application. Hence GrabPay will become a player in the FinTech Payment space. Their other offerings will probably be trying to use GrabPay to automate and aggregate all personal spending and perhaps to generate reporting solving certain aspects of “Financial Literacy” problem statements.

iCompareLoan.com

For Consumers

iCompareLoan.com is a loan comparison Finance portal comparing Mortgage Loan as well as other loans, it provides many user comparison tools and applications for consumers to find out more about themselves (Financial Literacy), such as TDSR analysis, mortgage insurance premium estimate, Retirement planning premium estimate, Car affordability analysis, Equity-term-loan estimate, etc. This site provides “Financial Analysis for home buyers” under Customer engagement, to help customers to make informed decisions.

Consumers also have the convenience of more automated using E-Signature and application form submission, automating the customer acquisition process under the “KYC and Identity authentication” space.

The site promotes financial education and prudence through fact based editorial. iCompareLoan is Singapore’s leading Mortgage Broker.

For Top Property Agents and Financial Advisor

Singapore’s first and only Cloud based Home Loan Report platform that automates mortgage planning analysis. This tool helps property agents to service their property buyers more professionally and assist in closing property deals faster and accurately as well as conduct listing presentation (Sellers mostly have 1 property, they will not sell if they do know if they can afford to buy the next property). Financial advisors can provide mortgage planning and analysis to complement the overall wealth planning and free up locked home equity to help customers to plan and grow their retirement wealth better. Automated Home Loan Reports helps increase consulting efficiency for agents as well as Advisors.

Is there a Future for FinTech?

Companies should continue to incrementally automate problems around workflows or system flow and need NOT totally follow MAS’ stratified problem statements.

FinTech (Blockchain) can complement or disrupt banks to become the creator of credit, aggregator and distributor of capital.

Block chain can become the technology behind e-wallets without the need for expensive accounting and backend operations. It can bring about peer-to-peer lending with social network verification for a low default rate, by-passing the banks.

Block chain technology and the payment segment will likely be the most fought after “Blue ocean”, and eventually become the most fragmented as defined with the various FORK, the most bloody, but the technology most likely to change the way we live, work and play. Regulation can slow it in some way, but some trends are not so easy to stop, instead the law should catch up and accommodate the new reality.

Singapore has a tiny market, but it can still play a leadership role globally as it has the infrastructure, a highly educated workforce, strategic vision and dare to allow us to reach the world with Singapore’s products. It can consider a lighter touch regulatory environment and better angel investor environment to allow creativity to flourish.

References

- MAS 100 FinTech Problem statements, http://fintechnews.sg/3268/fintech/mas-100-fintech-problems-to-solve