Singapore banks’ 1Q19 loan drawdowns expected to be well supported by developers, with full year bank loans growth projected to come between 4% to 6%, said a recent research by DBS.

Key summary points of bank loans:

- Industry loan growth for March 2019 shows strongest m-o-m uptick of +1.0% in nine months

- New housing loan limits granted continue to be slow post property cooling measures

- Fixed deposits show fastest growth in >10 years which may weigh on cost of deposits

- Continue to expect profit-taking in May (ex-dividend date)

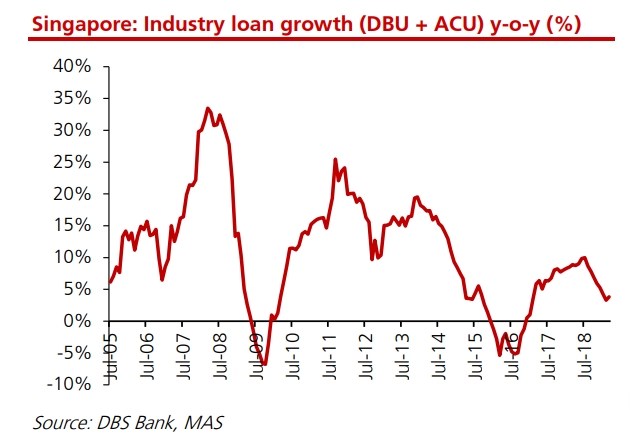

The report said that industry loan growth (DBU+ACU1) for March 2019 grew by +1.0% m-o-m/ +3.8% y-o-y, showing the strongest m-o-m uptick since June 2018, prior to the announcement of property cooling measures.

The strong m-o-m bank loans growth was largely driven by business loans (+1.2% m-o-m/ +4.8% y-o-y), especially manufacturing and general commerce loans.

The strong m-o-m bank loans growth was largely driven by business loans (+1.2% m-o-m/ +4.8% y-o-y), especially manufacturing and general commerce loans.

Table of Contents

Consumer bank loans reversed four months of negative growth and posted +0.4% m-o-m/ +1.0% y-o-y growth. Year-to-date, loan growth was +0.8%, said the report.

“New housing loan limits granted continue to be slow post property cooling measures. New housing loan limits granted continue to be slow at c$7.3bn for 1Q19, the lowest level since 4Q15, as the industry’s mortgage book continue to be largely flat amid ongoing mortgage repayments and slower new bookings. We expect business loans to continue driving loan growth for the year as mortgage drawdown remains slow.

“Supports our thesis that 1Q19 loan drawdowns for Singapore banks are likely to be well supported. As mentioned in our previous report (Singapore Banks: Expecting a better quarter), we expect the banks’ 1Q19 loan drawdowns to continue to be well supported by developers in relation to their en-bloc transactions, as well as other deal-related pipelines. We expect full-year loan growth for Singapore banks to come between 4% and 6%.”

Strong growth in fixed deposits (FD) may still weigh on cost of deposits, said the report. It added that FD growth of +20.0% y-o-y/+1.5% m-o-m may continue to weigh on the banks’ cost of deposits, as lower-cost CASA is progressively shifted into FDs. DBS continues to see moderate NIM expansion of c.2-5bps through FY19F.

“Continue to expect profit-taking in May (ex-dividend date); UOB remains our preferred pick. The banks will trade ex-dividend in May. Until then, the attractive dividend yields will continue to provide valuation support, though we expect some profit-taking closer to May.”

DBS announced in March that with effect from 4 March 2019, DBS FHR home bank loans pegged to DBS’ Fixed Deposit rates will be affected as the Fixed Deposit rates for the 7 to 48 months interest rates for SGD Fixed Deposit at DBS will be revised as follows:

DBS FHR Update – Fixed Deposit Rates Revised Upwards

| DBS FHR Fixed Deposit Rate For amounts $1,000 to $999,999 | ||

| Tenor | Existing (% p.a.) | New (% p.a.) |

| FHR Fixed Home Rate 7 months | 0.6750 | 0.9500 |

| FHR Fixed Home Rate

8 months |

0.6750 | 0.9500 |

| FHR Fixed Home Rate

9 months |

0.9500 | 1.3500 |

| FHR Fixed Home Rate

10 months |

0.9500 | 1.3500 |

| FHR Fixed Home Rate

11 months |

0.9500 | 1.3500 |

| FHR Fixed Home Rate

12 months |

0.9500 | 1.4000 |

| 18 months | 1.1000 | 1.4000 |

| 24 months | 1.2000 | 1.4000 |

| 36 months | 1.3000 | 1.4000 |

| 48 months | 1.3500 | 1.4000 |

Table 1: DBS bank revises their Fixed Home Rate (FHR), Home Loans Pegged to this Fixed Deposit Rate will pay more from 4th March 2019 onwards.

A fixed deposit (FD) is a financial instrument provided by banks which provides investors a higher rate of interest than a regular savings account, until the given maturity date. It may or may not require the creation of a separate account. It is known as a term deposit or time deposit in Canada, Australia, New Zealand, and the US, and as a bond in the United Kingdom and India.

The difference with fixed deposit is that the money cannot be withdrawn from the FD as compared to a recurring deposit or a demand deposit before maturity. Some banks may offer additional services to FD holders such as loans against FD certificates at competitive interest rates.

It is important to note that banks may offer lesser interest rates under uncertain economic conditions. The interest rate varies between 0.95 and 1.4 per cent.

DBS launched the Fixed Home Rate (FHR) home loans that are pegged to the fixed deposit rates in 2015, since then a new category of Home Loans pegged to the Bank’s fixed deposit rates is born. Generally referred to as the DBS FHR home loan packages.

The home loan interest rate are based on: –

- FHR + Spread = Housing Interest Rate

If the FHR rises, then the interest rate rises. Some of them may be using FHR (8 months), so just look at the 8 month FHR plus the spread stated in your contract, this will be your new rate.

How to Secure a Home Loan Quickly

Are you planning to invest in properties but ensure of funds availability for purchase? Don’t worry because iCompareLoan mortgage broker can set you up on a path that can get you a home loan in a quick and seamless manner. We are the experts who do the work for you for free, while you lean back, rest and rely on our professionalism at absolutely no cost to you.

Our brokers have close links with the best lenders in town and can help you compare Singapore home loans and settle for a package that best suits your home purchase needs. Find out money saving tips here.

Whether you are looking for a new home loan or to refinance, the Mortgage broker can help you get everything right from calculating mortgage repayment, comparing interest rates all through to securing the best home loans in Singapore. And the good thing is that all our services are free of charge. So it’s all worth it to secure a loan through us.

For advice on a new home loan.

For refinancing advice.