Have you heard of Dave Ramsey’s Debt Snowball Method?

By: Hitesh Khan/

A Debt Snowball is a debt elimination strategy popularized by Dave Ramsey, a renowned debt and personal finance guru. Under this method, you reduce your debt by paying the minimum monthly payment to all debts, except the one with the smallest balance, which you’ll try to pay down as fast as you can.

The basic steps in the Debt Snowball debt reduction plan are as follows:

- List all debts from smallest balance to largest. Note, there are people that advocates paying highest interest rate debt first, but that’s not the Debt Snowball method.

- Pay the minimum payment on every debt, except the smallest debt.

- Pay as much as you can towards that smallest debt until it is paid off.

- Once the smallest debt is paid in full, repeat the process by paying as much as you can toward the second smallest debt.

- The idea is that you’ll be able to pay more toward the “smallest” debt each time a debt is fully paid off.

https://www.icompareloan.com/resources/expat-personal-loans/

How Does Dave Ramsey’s Debt Snowball Work?

Table of Contents

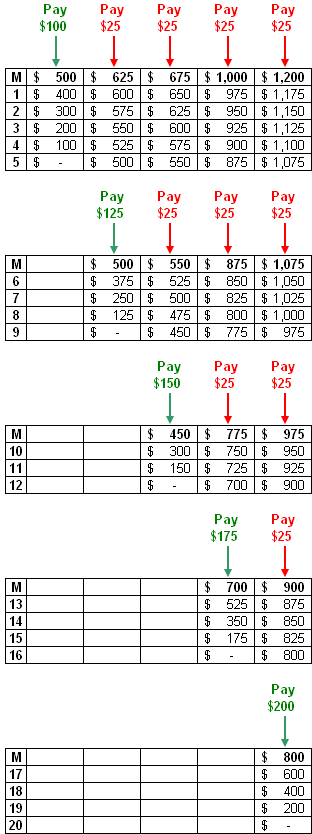

Let’s say you have 5 outstanding accounts in the following amount: $500, $625, $675, $1000, and $1200 — note, the interest rate is irrelevant. To keep this simple, let’s assume each debt requires a minimum payment of $25 per month, and ignore the increases in amount owed due to finance charges. Also, let’s assume you’ve budgeted $200 per months to pay off your debt.

The first month, you’ll pay $25 to all accounts, except the $500 one, which you’ll pay all of the remaining $100 budgeted. After 5 months, the $500 debt would be fully paid and the remaining ones are reduced to: $500, $550, $875, and $1075.

Now, you’ll repeat the same process by paying $25 to all, except the $500 one, which you’ll pay $125 per month ($100 from the original $500 debt that was paid off, plus the $25 you have been paying). After 4 months, the second debt is paid off (notice how it’s faster than the first $500), and the remaining debts are reduced to: $450, $775, and $975.

Rinse and repeat…

https://www.icompareloan.com/resources/urgent-loans/

An Illustration Of The Debt Snowball

Here’s the example in a table format to help you visualize the process.

Debt Snowball Variations

There are many variations of the Debt Snowball methods. Debt Snowflake, Debt Avalanche, Debt Deluge, are some of these variations.

Debt Snowflake

Debt Snowflake is debt reduction plan based on Debt Snowball, but the idea is to actively find and use additional income to pay even more than the budgeted amount toward your top priority debt. Debt snowflaking is about finding those extra small amounts of money to add to your debt snowball.

If you make a little extra money on the side, apply it toward debt. If you pay less for something than you normally would, apply the difference toward debt. If you’re tempted to buy something, but don’t, reward yourself by using the money you would have spent toward your debt. Over time, the money really adds up, and your little snowflakes add quite a bit to your debt snowball.

Debt Avalanche on the other hand, is similar to Debt Snowball, but the idea is to pay off the highest interest debt first. Some have claimed that mathematically, the Debt Avalanche is the “correct” method to choose over debt snowball. It may make sense since it will save you interest and it may save you some time too.

If you want to get out of debt, these steps can help you accomplish your goal more quickly and efficiently. Remember the key is to change your spending habits and not go further into debt, otherwise, you debt repayment plan will fail.

Once you have your spending under control, the key steps are to list your debt according to the interest rates, negotiate better terms with your lenders, find alternative funding sources to lower your interest rates, and to use Debt Snowball method to pay down your debt quickly.

Always remember to borrow only what you need and are able to repay. Be mindful that if you are unable to meet the contractual terms, the late payment fees and interest payment will be a financial strain not just on yourself but also on your family. You should not rush into and commit yourself to getting personal loans to get out of debts until you are sure that you can satisfy the terms and conditions.

How to Secure Personal Loans Quickly

If you are in a financial crunch and are searching for personal loans to expand your business, the loan consultants at iCompareLoan can set you up on a path that can get you a it in a quick and seamless manner. Our loan consultants have close links with the best lenders in town and can help you compare various loans and settle for a package that best suits your needs. Find out money saving tips here.

Our Affordability Tools help you make better property buying decisions. iCompareLoan Calculators help you ascertain the fair value of a property and find properties below market value in Singapore.

If you are looking for a new home loan or to refinance, our Mortgage brokers can help you get everything right from calculating mortgage repayment, comparing interest rates all through to securing the best home loans in Singapore. And the good thing is that all our services are free of charge. So it’s all worth it to secure a loan through us for your business expansion needs.

Contact us for advice on a new home loan.

Contact us for home loan or refinancing advice.