Floating rate home loan packages are often lower than fixed rate ones – but not always

By: Phoenix Lee/

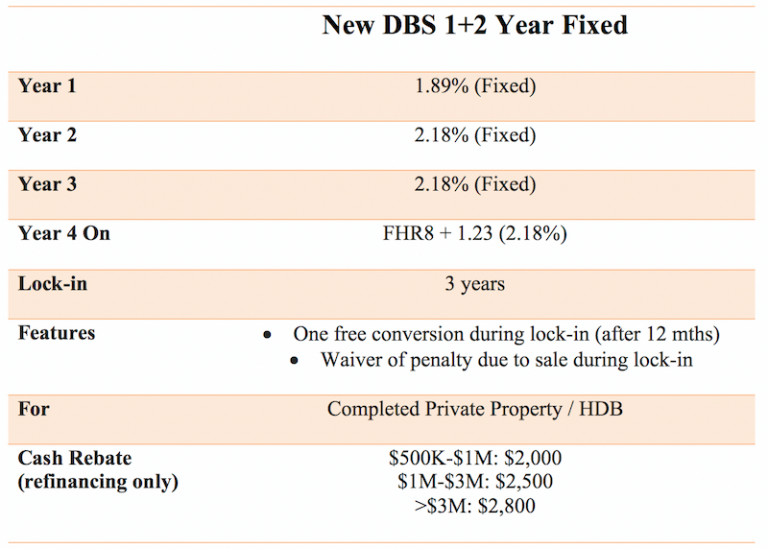

DBS, a leading mortgage loan lender, in July launched a National Day home loan promotion which offers a fixed rate home loan package with an introductory rate of 1.89% in the first year.

1+1+1 Fixed Rate Package

The DBS fixed rate home loan package offers free conversion to any prevailing loan packages during Year 2 or 3 of their loan.

| Year 1: | Year 2: | Year 3: |

|---|---|---|

| 1.89% p.a. | 2.18% p.a. or any prevailing loan package | 2.18% p.a. or any prevailing loan package |

| Thereafter |

|---|

| FHR8 + 1.23% p.a. |

Floating rate home loan packages With 1-Year Lock-in

| Year 1: | Year 2: | Year 3: |

|---|---|---|

| FHR8 + 1.13% p.a. | FHR8 + 1.13% p.a. | FHR8 + 1.13% p.a. |

| Thereafter: |

|---|

| FHR8 + 1.13% p.a. |

FHR8 refers to DBS Bank’s prevailing 8 months Singapore Dollar fixed deposit rate for amounts between S$1,000 and S$9,999 or such other sum as they may specify. It is currently 0.950% p.a.

The Chinese Daily Zaobao reported some months that besides DBS, two other banks have introduced a fixed rate home loan package which is lower than the floating rate home loan packages.

Table of Contents

Chief Mortgage Officer at iCompareLoan, Mr Paul Ho, speaking on the floating rate home loan packages offered by the various banks said, “I am not surprised by the rates falling to the >2% level. When clients come direct to us to find the best home loan for them, very often we will be able to find them an even better rate than what they will find on the internet.”

Home owners tend to balk at fixed rate home loan package because it is more expensive. They want to take floating rate home loan packages that is cheaper than a fixed rate package and then hope that floating rate will not rise.

Generally, when the mortgage interest rate upward trend has been established, the fixed rates would have moved even higher. Home owners on floating rate packages then start to receive letters from banks informing them of the new increased rates. Many will be shocked and upset.

Fixed rate home loan package are almost always more expensive than floating rate home loan packages.

https://www.icompareloan.com/resources/mortgage-broker-singapore-best-rate/

As banks are unsure of the future interest rate environment, they will need to enter into hedging contracts, which incur a fee, to guarantee you the future rates. It’s like buying an insurance policy against interest rates going crazy.

For example, if the current borrowing cost of the bank is 1.5%. The bank may then decide to create a fixed rate package that is 2% fixed for 3 years.

However, the bank does not know what will happen in year 2 and year 3. What if the cost of borrowing for the bank rises to 3% for year 2 and 3?

This would mean that the bank’s profit would be: –

- Year 1 = 2% – 1.5% (cost of funds) = 0.5%

- Year 2 = 2% – 3% (cost of funds) = -1%

- Year 3 = 2% – 3% (cost of funds) = -1%

- Total over 3 years = -1.5%

A bank is unlikely to create a product that has a risk of losing money. So banks typically pay a fee to go into a hedging contract.

https://www.icompareloan.com/resources/mortgage-type/

The bank will buy a hedging product that would guarantee them 2% for year 2 and year 3 and maybe pay a fee of maybe 0.3% to do so. It is similar to insurance.

Hence the bank’s profit would be: –

- Year 1 = 2% – 1.5% (cost of funds) = 0.5%

- Year 2 = 2% – 1.5% Cost of funds + 0.3% Hedging cost = 0.2%

- Year 3 = 2% – 1.5% Cost of funds + 0.3% Hedging cost = 0.2%

- Total (over 3 years) = 0.9%

A guaranteed profit for each mortgage loan product is probably more important for the bank than the potential to make more money, but also open to the possibility to lose money.

Mr Ho said, “sometimes we have customers who come to iCompareLoan and say, ‘Find me a home loan that is fixed. I want a fixed rate for the entire tenure of my loan’, but currently there are no banks that offer a perpetual fixed rate for the entire loan tenure.”

He added, “a fixed rate home loan package is typically fixed for between 1 to 5 years of the loan tenure. After the fixed rate period ends, the subsequent years revert back to floating rates.”

“Many people are confused. They tell us they got a 36 months fixed rate mortgage very cheaply. Upon closer investigation and to their horror, it was not a Fixed Rate for 36 months, it’s a Floating Rate package pegged to the 36 months fixed deposit rate.”

Mr Ho said, “customers should go directly for a fixed rate home loan package if the difference with the floating rate is not very much more expensive.”

If you are planning to invest in properties but are ensure of funds availability for purchase, you should speak to a mortgage broker who can set you up on a path that can get you a home loan in a quick and seamless manner. Most mortgage brokers have close links with the best lenders in town and can help you compare Singapore home loans and settle for a package that best suits your home purchase needs. Before you set out to find the best home loans, you should find out about money saving tips as well.

Whether you are looking for a new home loan or to refinance, mortgage brokers can help you get everything right from calculating mortgage repayment, comparing interest rates all through to securing the best home loans in Singapore. And the good thing is that all their services are free of charge. So it’s all worth it to secure a loan through them. They can also give you good refinancing advise, which could help you save thousands of dollars.