OCBC follows hot on the heels of DBS and UOB to launch a new fixed deposit rate pegged package

Paul Ho (iCompareLoan.com) 07 Aug 2017.

A bit of recap of how all such rates came about.

DBS created the market’s first Pegged to Fixed Deposit Rate package in 2014. They called in Fixed Home Rate. Please note that “Fixed Home Rate” is not a “Fixed Rate” package, it is a variable rate pegged to the fixed deposit rate, perhaps it is a misnomer that confuses many.

Here is a history of FHR FDMR FDPR pegged to fixed deposit rates.

Recently DBS changed their Fixed Deposit rate peg from 12/24-month fixed deposit to 9-month fixed deposit on 3 April 2017. This means that, for the same rate of say 1.3% which is made up of FHR (12/24) at 0.6% + 0.7% the spread is higher, because it becomes: –

- FHR (9-month) at 0.25% + 1.05% = 1.3%. (Where 1.05% is the spread)

We also speculated that OCBC will follow suit soon. On 18th July 2017, OCBC launched switched their reference from pegged to their 36-month Fixed Deposit to 15-month Fixed deposit. UOB has also similarly made the switch from referencing their 36-month Fixed deposit Pegged Rate (FDPR) to using 15-month fixed deposit pegged rate (FDPR) in May 2017, soon after DBS.

Fixed Deposit Mortgage Rate Terminology

Table of Contents

DBS calls their product “Fixed Home Rate” or (FHR).

UOB calls their product “Fixed deposit Pegged Rate” or (FDPR).

OCBC calls their product “Fixed deposit Mortgage Rate” or (FDMR).

They all mean the same thing.

Before OCBC’s switch

- FDMR (36-month) at 0.65% + 0.65% = 1.3% (Where 0.65% is the spread)

After OCBC’s switch (18th July 2017)

- FDMR (15-month) at 0.25% + 1.05% = 1.3% (Where 1.05% is the spread)

It could be that bank could be transferring the interest rate risks to the consumer.

The reason for that is, the lower tenure rates, be it savings/deposit rates or interest rates or lending rates, the lower tenure ones tends to be more volatile. This means that these rates may have a tendency to bahave more closely with the market interest rates, namely the Sibor and the Sor rates.

This also means that the perception that variable rates that are pegged to Fixed deposit rate being safer will undergo a re-evaluation as these rates tend to move a bit more actively compared to the higher tenure fixed deposit rates.

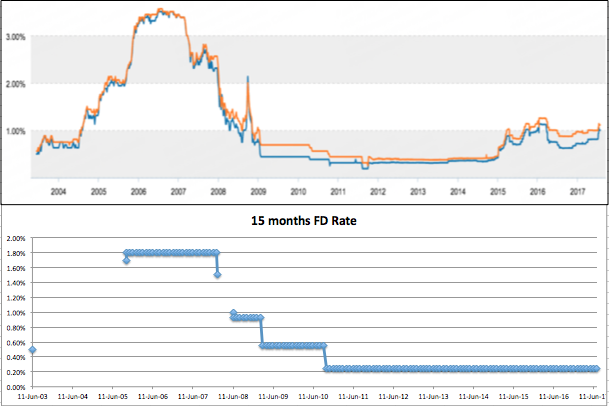

What is the Historical movement OCBC’s 15-month fixed deposit rate?

We have collated the Chart and movement for OCBC’s 15-month Fixed Deposit rate, (Magnitude on vertical axis only approximately to scale).

Chart 1: 1-month and 3-month Sibor versus 15-month OCBC Fixed Deposit Rate from 11 Jun 2003 to July 2017, ABS, OCBC, iCompareLoan.com

As you can see in this previous article of OCBC’s 36-month Fixed deposit rate, the 36-month Fixed Deposit rate is far less responsive to the market interest rate movement of the Sibor.

Now that DBS, UOB and OCBC has switched to a shorter tenure fixed deposit reference, we are almost certain that the banks perhaps know something that we do not, that the interest rates are now set to rise.

If the 3 banks are correct, that also means that those who bet on fixed rates now, may be correct. Some of the more attractive Fixed rates are from Citibank, HSBC and Bank of China at the time of publishing. However it is not applicable for all property types.

For the uninitiated, you may want to speak to a mortgage broker who can work you through all the calculations, regulations and home loan selection scenarios.